In 2016 General Electric (GE) sold its domestic appliances division to Haier from China. The American company reached a dismal situation wherein it needs to repay a large debt and streamline its businesses. Selling the consumer-oriented business may have seemed to the management, led at the time by previous CEO Jeff Immelt, as a means to relieve the company from a business that is out-of-line with its other mostly industry-oriented business areas. However, that division was an asset whose value could not be measured just in financial terms — it was more than a capital asset. It provided a valuable support to the brand of General Electric, together with the lighting business. The incoming CEO John Flannery is planning even more drastic changes to the company’s composition, but removing the appliances division might turn out as an obstacle to his mission. The industry brand of GE could benefit from its long appraised consumer brand.

General Electric is engaged in a range of business areas. In some of them the company has obtained or enhanced its capabilities through acquisitions during the tenures of CEOs Jack Welch (1981-2001) and Jeff Immelt (2001-2017). The businesses of GE feature: (1) Additive –advanced manufacturing technologies (e.g., 3D printing); (2) Aviation — engines, components and electric systems for jets, and avionics (e.g., innovative digital pilot dash-boards); (3) Power, including gas, steam and nuclear power; (4) Industrial Connections, including electrification, grid and control; (5) Healthcare — medical technologies such as ultrasound, MRI & CT, digital integrated care (i.e., data sharing and management), patient monitoring, surgical imaging and more; (6) Renewable Energy, including wind, solar and hydro, and innovative hybrid solutions; (7) Transportation — digital automation and industrial Internet-of-Things (IoT) solutions for locomotives, marine (drilling) and mining. The businesses of GE today are directed largely to industrial, commercial, and public clients. The last business that targets consumers at least in part is Lighting, offering advanced LED bulbs (e.g., smart IoT-controlled, HD-quality), linear fluorescents, and other products.

Noteworthy, digital transformation is omnipresent through most of the businesses of the company, entailing advanced computer-based digital systems, interfaces, and mobile applications (e.g., IoT apps developed in co-operation with leading hi-tech companies). Much of the digital activity seems to be originated, planned and developed at the Digital division or unit of the company (e.g., industrial apps serving IoT products, Predix — the online platform applying IoT data and predictive analytics, manufacturing software, as well as cybersecurity). Internet-of-Things functionality applies also to lighting products for consumers; it was supposed to be implemented as well in their domestic appliances. In practice, the appliances may still be reliant on GE for IoT technology even after the transition.

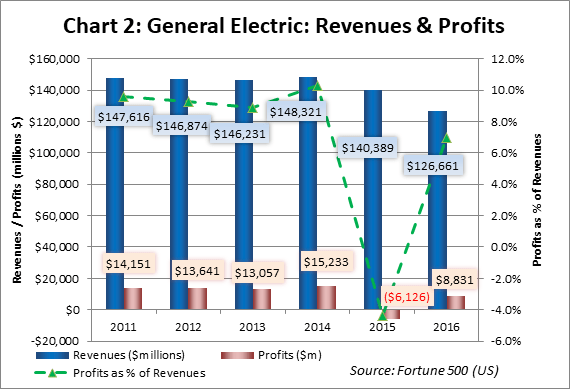

For many years the Appliances of GE were commonly associated by consumers with quality and durability — having a refrigerator carrying the art-graphic logo sign of GE in the kitchen was taken as a symbol of social status. In 2015 the appliances division generated revenues of $6.34bn, 7.1% of GE’s total revenues. The combined revenues of GE from appliances and lighting, as reported by the company, stood at $8.8bn (an increase of 4.8% from the previous year). Combined profits were $700m, a margin of 7.7% as percentage of revenues (GE 2015 report on financial results, Segment Operations: Appliances and Lighting). GE overall reported a loss in 2015 (see Chart 2). The company first tried to sell its appliances to Electrolux but the deal was objected by the American Department of Justice. A new process for selling the division started with Qingdao Haier, and after six months of negotiations a deal was closed in June 2016 at a price of $5.6bn. The range of appliances in their new ‘home’ includes refrigeration, cleaning (dishwashers), cooking, laundry (washing machines), accessories such as water filters, and air-conditioning.

The division of appliances is now identified as ‘GE Appliances: A Haier Company’. This company is in an interim period of transition, alas outwards its status creates a bit of confusion about who is really in charge. The company’s website is resident at a domain titled ‘geappliances.com’ and the company retains the brand identity of GE. The association with Haier does not seem too committing. For example, whom consumers should expect to be responsible for their appliances? Or, how to distinguish between appliances that originate from GE or from Haier? The headquarters of GE Appliances remains for the time being in US territory in Louisville, Kentucky, under American executive leadership. Recently, the new company announced the creation of appliance connectivity — operation command by voice and through mobile apps (IoT). Yet the technology is reasonably a direct extension of GE’s development of capabilities of Artificial Intelligence and IoT in their businesses for industry.

Haier has thereof received a strategic foothold on US soil, in hope to strengthen its position in the country and establish a long sought market share in the American market; American consumers have refrained from buying appliances of Haier. The Chinese manufacturer rose from a failing refrigerator factory in Qingdao of thirty years ago by instilling over time quality standards that were much higher than those accustomed in China. Zhang Ruimin, leading the transformation, succeeded remarkably in turning the company into a major national appliances manufacturer in China with global extensions. However, the quality standards at Haier remain behind those of developed countries and therefore the company’s efforts to sell in the ‘West’ have been lingering (1). Haier still has a challenge of closing a gap in quality and credibility, which the acquisition from GE is expected to help overcome. Many consumers in the US as well as in other Western countries will probably remain concerned by ambiguity about the source of their appliances, being of GE (United States) or Haier (China). Haier also gained important American technological know-how (e.g., in AI) from the American company. General Electric apparently gained a financial relief, but one that may be only for a short-term, and the company may have to pay for it in the future.

The new CEO of GE, John Flannery, revealed in an annual ‘Investor Day’ meeting last month (Nov. ’17) the company’s plan to focus on three business areas: power, aviation, and healthcare. It will exit completely some of its existing business operations (e.g., transportation, lighting, industrial solutions, electrification) while reducing its effort and involvement in others. For example, the company will retain its digital unit or division to develop and sell apps to customers for operating and monitoring equipment reliant on Predix platform, yet with a smaller budget. Flannery was less clear on the future of some areas such as renewable energy where the company is not completely willing to leave and some other arrangement may have to be found. Strategically, the plan is to reduce the span of businesses the company engages. In addition, the CEO informed analysts that the company will have to cut in half its dividends.

The share of GE climbed from a level of $25 to $30+ in late 2015 and held its price as high through 2016 with small fluctuations. Then, the price started to slip down continually through 2017. So much for the effect of selling GE Appliances on equity. By August 2017 the share price already came back to $25. Since Flannery entered the CEO office, and subsequently following the announcement of his plan and the harsh cut in dividends, the share price steeply fell to about $18, as low as the band of $15-20 in which the share fluctuated in 2009-2011.

Analysts were left unsatisfied and critical about the turnaround plan at GE. They complain for instance that the company is too expansive, and that it must increase efficiency and reduce duplicate costs across the organization (Reuters, 13 Nov. ’17). Others express concern in particular about the debt at GE, and that the plan includes insufficient measures to fix problems with the company’s businesses (CNBC.com, 14 Nov. 2017 — also noted, GE share underperformed S&P 500). Part of the cure will have to include exit from some businesses (e.g., where GE entered by acquiring another company or where it did not build a substantial advantage). Nevertheless, increasing efficiency and reducing duplicate costs can be achieved also by merging some associated areas and consolidating them into a new division, though perhaps narrowing the scope of operation in each field. One example for doing so may be in the area of energy: sources, production or distribution (i.e., power, renewable energy, connections). Another area to consider is ‘digital’ — balancing between development of original technologies and solutions in a central unit, and their implementation for specific systems and equipment in the various business divisions. Letting go of the appliances business could be seen as a logical way to free resources for advancing industry-related areas of expertise that remain. But solving problems of over-expansion and inefficiency in the industry-oriented businesses did not have to come at the expense of the consumer-oriented business in which the company developed product and brand advantages over decades.

The company has to come to terms now with damages from excessive expansion-by-acquisition, a strategy led by Welch and followed by Immelt. The ‘elephant in the room’ for the company is GE Capital, the investment bank of General Electric, whose troubles particularly since 2009 inflict on the whole company. Now the company under Flannery plans to heal by letting go of some more of its genuine businesses such as transportation and lighting (Matt Egan, CNNMoney.com, 20 Nov. ’17), that is, in addition to the appliances already shed by Immelt. The company has built an expertise in transportation, especially locomotives, during the past hundred years. Lighting can be regarded as a founder’s asset of the company (i.e., attributed to Thomas Edison); as described by Egan, lighting “symbolizes the company’s history of innovation”. General Electric could find it very difficult to continue after removing parts of its heart and soul.

The intensive occupation of the company with allocation of capital was initiated and developed by Welch but it spiralled out of control under the leadership of Immelt. The latter quadrupled the amount of capital invested in the company (from $42bn in 2001 to $163bn in 2009) which involved a significant increase in borrowing. By 2011 it was recognised as a major problem with the management of Immelt. Geoff Colvin of Fortune described how Immelt as CEO remade the portfolio of GE, for instance by entering new “future industries” (e.g., healthcare, green energy). However, his aggressive expansion came at a high cost. While the CEO already tried to unburden the company from some businesses (e.g., NBC and Universal Studios), it was seen by analysts as insufficient. The real issue at GE, as Colvin noted, was capital allocation, and it became more so critical at GE Capital (2). The decision to quit the involvement of GE in TV broadcasting and online media (NBC) as well as cinema productions (Universal) sounds very reasonable. Conversely, the claim supported also by Colvin that Immelt was waiting too long to unload appliances (executed only in 2016) and lighting (never completed to-date) from GE should be much less applauded because these business areas made-up a distinct branch at GE with deep roots, and were also carriers of its consumer brand, a valued non-tangible asset.

In a highly critical opinion column in the Financial Times, John Gapper argues that focusing management on capital allocation could kill GE as an industrial company. It would make GE operate more like an equity fund. The company needs to shift because it may no longer be sustainable to run a manufacturing conglomerate as in the 1980s. However, it does not require to treat the business units as equity holdings for capital optimization: “Once efficient allocation becomes the priority, it is hard avoid this cycle.” It cannot be surprising for Flannery to continue this path, following the leadership of Welch and Immelt, considering his long career at GE Capital, up to the latest post he held as head of that division. Culture and a style of management have kept the units of GE stick together like a glue for many years. Without them, Gapper wonders how longer GE can hold together (FT.com 15 Nov. ’17).

The financial figures of GE in 2015 and 2016, as published in the Fortune 500 ranking, show little so far in favour of the impact of exiting from some business activities such as Appliances, measures taken by Immelt to heal the company in his last years in office: The revenues have fallen, but moreover the return on revenues has also decreased from a level of 8%-10% in 2011-2014 to 7% in 2016, after recovering from a loss in 2015 (Chart 2 below). It should be noted nonetheless that the value of assets has already shrunk by 50% between 2011 ($717bn) and 2016 ($365bn).

-

General Electric descended from former 6th-9th positions in the ranking of Fortune 500 (US) to 11th place in 2015 and 13th in 2016.

The products of GE for consumers, both appliances and lighting devices, were the ‘face’ of the company to the wide public and a closer form of connection with consumers. Their contribution is in providing stability and longevity to the GE brand, identified by name, logo, and other associated elements. Above all, the brand was represented in products, equipment and devices, in millions of homes, to be useful in the everyday lives of the consumers and make their lives more comfortable. The domestic products also were a channel to implement some of the technological progress and innovation of the company and demonstrate them to a wider public audience. Consequently, exposing consumers (who also happen to be small investors) to GE could help to increase public confidence in the company, especially in turbulent times.

General Electric did not depend on the appliances and may do well without that business. The same may be true for the lighting business. But removing them will not bring the cure either– the selling of GE Appliances apparently has gone wasted so far. Instead, keeping the consumer products would have enhanced the corporate brand. The management could perhaps have gained some peace of mind while reforming their industry-related businesses. In the medium term, making reforms could be a little harder for Flannery and his top-management team to push through. In the longer term, leaving consumer products out of the company — as already happened with the appliances and is expected to repeat with lighting — may remain as a wound, something amiss, in the reputation and brand image of General Electric.

Ron Ventura, Ph.D. (Marketing)

Notes:

(1) “Zhang Ruimin’s Haier Power”, Michael Schuman, Time (Europe), 14 April 2014 (183 (14)).

(2) “Grading Jeff Immelt”, Geoff Colvin, Fortune (Europe), 28 February 2011 (163 (3)).

Thought provoking analyis of GE’s situation